A profitable business can still run out of cash. I know that sounds wrong, but it’s one of the most common cash flow problems I see.

CB Insights puts the share of startups that run out of cash at 38%. Cash flow problems in small businesses don’t come from a lack of revenue, but rather from not diagnosing the actual cause.

That’s exactly what this blog is for. I’ll walk you through 12 common cash flow problems, what’s behind each one, and how to fix them directly.

1) Late payments from customers

The work gets done, the invoice goes out a few days later, and no one follows up until after the due date. By that point, a net-30 term has already stretched into 45 or 60 days. According to QuickBooks, 56% of small businesses are waiting on unpaid invoices at any given time.

What surprised me early on was that stricter terms don’t always fix this. Moving from net-30 to net-15 sounds right, but it usually adds friction without changing behavior. What works better is changing when you get paid. A simple shift to 30-50% upfront and the rest before final delivery improves cash timing without negotiation.

Four changes fix most late-payment problems:

- Invoice immediately. Even a 2-3 day delay pushes your entire cycle back.

- Follow up before the due date. A reminder 3-5 days before, one on the due date, then escalate. Most people wait until it’s late. That’s already too late.

- Keep invoice language simple. “Pay within 21 days” works better than formal terms.

- Tie payments to milestones. Don’t wait until the entire project is done to bill.

Late payments are more predictable than most people realize. They usually come from the same types of clients, and poor cash flow management is consistently one of the reasons why small businesses fail.

2) Expenses growing faster than revenue

One of the most overlooked causes of cash flow problems is expenses growing faster than revenue. Rent, salaries, software, and insurance keep compounding regardless of what’s coming in. Each line item looks manageable on its own, so the combined growth goes unnoticed.

WeWork is the most documented version of this at scale. In 2018, the company doubled revenue to $1.8 billion. Losses doubled too, hitting $1.9 billion the same year. By mid-2019, total expenses were running at 190% of revenue. Revenue kept climbing. The business kept bleeding.

The fix is knowing which costs are actually growing. A simple three-step audit usually surfaces it:

- List every recurring expense, monthly and quarterly.

- Calculate each as a percentage of revenue.

- Flag anything that grew faster than revenue over the last quarter.

The categories that keep coming up are: SaaS subscriptions that quietly stack over time, contractor costs tied to growth, insurance renewals, and fixed overhead. Pick the top three line items growing faster than revenue and either cut them or renegotiate them this quarter. That single action closes most of the gap.

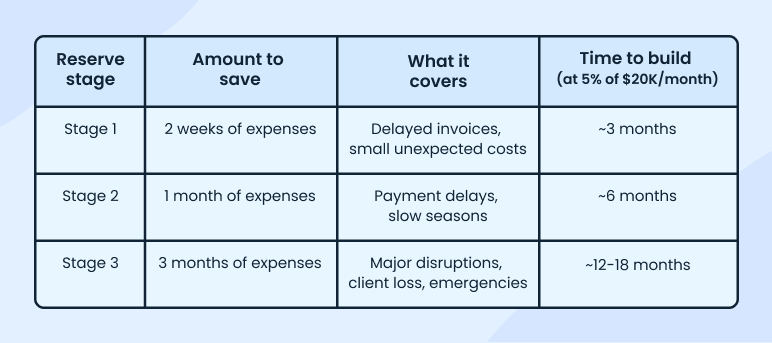

3) No cash reserve for emergencies

What happens when your biggest client delays payment by 60 days and there’s nothing set aside to cover that gap? For most small businesses, that’s not a hypothetical. According to a 2016 JPMorgan Chase Institute report, the median small business holds just 27 days of cash reserves.

Most advice on this jumps straight to “save 3-6 months of expenses.” I get why that’s the recommendation, but it’s not useful when cash is already tight. What works better is building in stages.

The method I’d recommend is tying savings to incoming cash rather than setting aside a fixed amount each month. Put 5% of every payment received into a separate reserve account. Once the first milestone is hit, increase that to 10%.

4) Seasonal revenue swings

Landscaping peaks in summer, retail spikes in Q4, and tax services cluster around filing season. Rent, payroll, and insurance don’t fluctuate with it. Those stay constant while revenue drops 30-60% in off-months.

Data from the U.S. Census Bureau shows that November and December alone account for roughly 19-20% of annual retail sales, and significantly more for gift-heavy categories.

A few ways you can combat the seasonal revenue swing are by:

- Setting aside a fixed percentage of peak revenue specifically for off-season fixed costs.

- Introducing off-season offers: maintenance packages, early booking discounts, bundled services to keep some cash moving.

- Negotiating more flexible payment terms with vendors during slower periods.

- Mapping the gap with a 6-12 month forecast so shortfalls are visible before they arrive.

5) Poor cash flow forecasting

Cash flow forecasting feels complicated. But the mechanics are straightforward. You have to map when cash comes in and when it goes out, then spot the gaps before they become emergencies.

Amazon is the most cited example of cash flow planning done well. The company collects from customers before paying suppliers, which creates a strong cash position despite heavy ongoing investment. The Harvard Business Review has covered this approach in detail.

Building a basic forecast takes three steps:

- List expected inflows by week or month: customer payments, deposits, and any other incoming cash.

- List expected outflows: payroll, rent, subscriptions, supplier payments.

- Calculate the net position each period and flag any week where cash goes negative.

If you want something that updates automatically as inputs change, Upmetrics’ cash flow forecasting tool handles this without manual tracking.

For a deeper understanding of how forecasting works, our guide on what is cash flow forecasting is a good starting point.

6) Inventory tying up working capital

Inventory can make your business look strong while quietly draining cash. Every time you buy stock, cash leaves your account before any revenue comes back. If you spend $50,000 on inventory, that money is locked until it sells. If it moves slowly, your cash stays stuck for months.

In 2022, Nike’s inventory jumped roughly 44% year-over-year to $9.7 billion as demand slowed. To free up cash, the company was forced into heavy discounting, taking a direct hit to margins in the process.

A simple way to track this is inventory turnover:

Inventory Turnover = Cost of Goods Sold ÷ Average Inventory

The healthy range for many retail businesses is 8–12 times/year. Below 4 usually means cash is tied up too long.

A few practical ways to fix this:

- Order closer to demand: Avoid buying large quantities too early unless there’s clear demand.

- Identify slow-moving items: Discount or bundle them to convert stock back into cash.

- Negotiate supplier terms: Consignment or delayed payment reduces upfront cash pressure.

7) Overdependence on a few clients

If one client makes up a large share of your revenue, it doesn’t feel risky at first. It feels efficient. The problem shows up the moment that the client delays payment, cuts their budget, or leaves.

Cash flow drops immediately, and expenses don’t adjust with it. A common rule of thumb and widely used by business bankers is to keep any single client below 25% of revenue. That said, the right threshold depends on contract length, payment reliability, and how quickly you could replace that revenue if the relationship ended.

The fix is to reduce dependence over time:

- Set an internal cap and avoid letting any single client grow beyond 25% of total revenue.

- Actively pursue new client segments rather than deepening concentration with existing ones.

- Build recurring revenue through retainers or subscriptions. Even one retainer client covering core monthly expenses changes how exposed the business is.

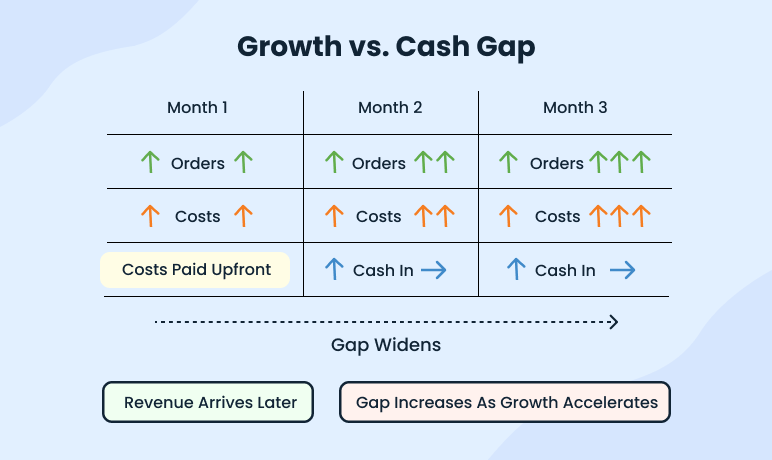

8) Rapid growth outpacing cash

Growth means more orders, more demand, and more revenue on the horizon. It also means higher upfront costs: materials, hiring, equipment, all of it paid before the revenue actually arrives. The faster the growth, the wider that gap becomes.

You can see a version of this at a larger scale with Quibi. The company raised nearly $1.75 billion and invested heavily in content and operations before building sustainable revenue. It shut down within a year.

The fixes are about timing:

- Require deposits or milestone payments on larger contracts. A 30-50% deposit shifts the cash burden back to the client before work begins.

- Phase your scaling. Don’t build capacity for the next stage until the current stage is generating cash.

- Secure a line of credit before you need it. Lenders approve based on financial health, not urgency. Apply when things look good.

Growth itself is not the problem. The timing of cash is.

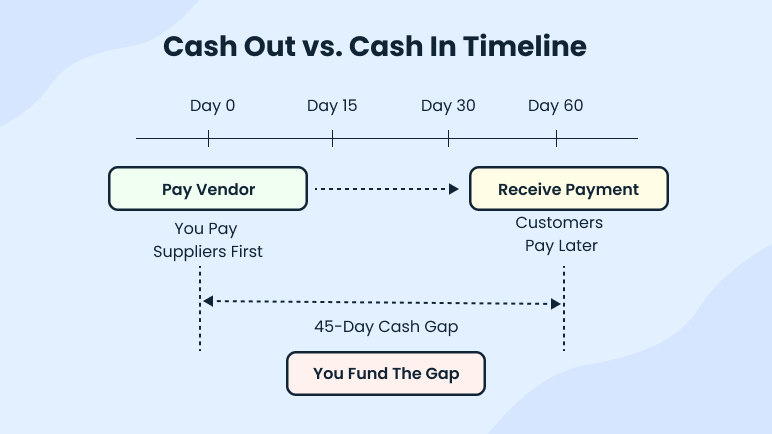

9) Unfavorable payment terms with vendors

You might be paying suppliers in 15 or 30 days, while your customers take 45 or 60 days to pay you. It means you’re covering the cost of operations before the cash actually comes in, and that gap repeats every cycle.

If the outflow happens earlier, the business has to absorb that gap every month. In my experience, simply asking a supplier to move from net-15 to net-30 frees up two weeks of working capital without changing anything else.

Many suppliers will consider the extension, particularly if you can offer a volume commitment or absorb a small 1-2% price adjustment in exchange. It won’t always work, but it’s a conversation worth having before assuming the terms are fixed.

A few adjustments that consistently help:

- Ask for extended terms. Net-30 or net-45 from suppliers is a reasonable ask for consistent accounts.

- Align payment timing. Try to pay vendors on the same schedule that your customers pay you.

- Use order volume when negotiating. Consistent, predictable orders give you more room to negotiate than you might think.

Even shifting one supplier by 15 days can meaningfully reduce the pressure on your operating cash.

10) Low profit margins masking cash shortfalls

Low profit margins are one of the least obvious cash flow issues a business can have. A delayed payment, a slow week, an unexpected cost; each one creates immediate pressure because there’s no buffer built into the numbers.

According to NYU Stern’s industry margin data, retail and grocery businesses often operate on very thin net margins despite high revenue volumes. These are rough gross margin benchmarks by industry:

- Retail: 25-50% gross margin

- Service businesses: 50-75%

- SaaS: 70-85%

Gross margin tells you how much is left after direct costs. But cash flow pressure comes from net margin, which is what’s left after rent, payroll, and overhead. A retail business at 40% gross margin can still run out of cash if net margin is 3-5% and a single payment arrives late. That’s the buffer that matters most.

If you’re consistently below these ranges, the business doesn’t have enough cushion to handle normal disruption.

In most cases, I work through, thin margins trace back to a combination of the same three things, and each has a direct fix:

- Pricing hasn’t been reviewed in over a year: A simple audit of your rates against current market pricing is usually enough to identify the gap.

- Supplier costs haven’t been renegotiated: A direct conversation with two or three vendors about volume discounts or extended terms can improve margins without touching revenue.

- The 80/20 problem: Twenty percent of products or clients typically generate 80% of profit. Identify the bottom 20% by margin and either reprice them or cut them.

For testing pricing scenarios against your financials, Upmetrics’ financial modeling tool makes this easier to work through.

11) Mixing personal and business finances

When personal and business expenses run through the same account, it becomes difficult to understand what’s actually happening with cash. A low balance could mean the business is struggling, or it could just be personal spending.

There’s no clear way to separate the two, which means every decision you make about hiring, spending, or investing is based on distorted numbers.

The cash flow problem is only part of it. Co-mingling finances also creates tax risk. Mixed accounts make it harder to claim legitimate business deductions, and in the case of an audit, the IRS treats unclear records as a red flag.

For LLCs and corporations, mixing personal and business funds can pierce the corporate veil, meaning personal assets lose their legal protection.

Three steps fix this immediately:

- Get an EIN and open a dedicated business checking account.

- Get a business-only card. This alone makes bookkeeping and tax prep significantly faster.

- Pay yourself a fixed monthly salary. A fixed salary makes your personal finances predictable and keeps business cash flow predictable.

The salary question comes up constantly. A reasonable starting point is what you’d pay someone else to do your job. It doesn’t have to be market rate immediately, but it should be a fixed, consistent number that appears as a real expense in your books.

12) Unplanned large purchases

Most large expenses aren’t surprises. Equipment ages, leases renew, upgrades become necessary. The issue isn’t the purchase itself. It’s that most businesses don’t plan for it until the bill arrives.

A $20,000 equipment replacement can wipe out months of reserves in a single transaction, while everything else, payroll, rent, and suppliers, keeps running as normal. That’s what makes it disruptive.

The fix is treating large purchases as a line item, not an emergency. I keep a simple capital expense schedule: every major asset, its expected lifespan, and a rough replacement cost. That alone changes how these decisions get made.

Two things that reduce the impact:

- Set aside a fixed monthly amount specifically for capital expenses.

- Compare buying versus leasing for high-cost items. Leasing spreads the cash impact over time.

For a deeper breakdown, you can refer to our guide on how to plan major purchases.

How to prevent cash flow problems before they start

What I’ve found is that a simple system, followed consistently, removes most of the risks we discussed. Here are a few:

- Maintain a 13-week cash flow forecast. Update it weekly so you can see gaps early.

- Set aside 5-10% of every payment. This builds a reserve without needing large one-time savings.

- Review receivables regularly. Anything overdue should be visible and acted on quickly.

- Check expense trends monthly. Look for categories growing faster than revenue.

- Track your cash runway. Know how many months you can operate with current cash.

None of these steps is complex. Dealing with cash flow problems becomes significantly easier once you have a system running consistently. Once you can see your cash flow ahead of time, most decisions become easier, and fewer problems catch you off guard.

For the habits that keep forecasts useful over time, our cash flow forecasting best practices guide is worth bookmarking.

Conclusion

The 12 cash flow problems and solutions covered here show up across most businesses, whether it’s delayed payments, rising costs, poor planning, or uneven revenue. Once you have a clear view of your cash flow, especially through a simple forecast, the same business cash flow problems become easier to manage or avoid altogether.

Knowing how to solve cash flow problems starts with visibility. Knowing how to create a cash flow statement gives you the foundation. Put a system in place, follow it consistently, and build from there. If you want to simplify the process, tools like Upmetrics can help you forecast your cash flow, track gaps, and stay ahead instead of catching up.

SCORE.org also offers free mentorship and cash flow resources if you want hands-on guidance alongside the tools.

The Quickest Way to turn a Business Idea into a Business Plan

Fill-in-the-blanks and automatic financials make it easy.